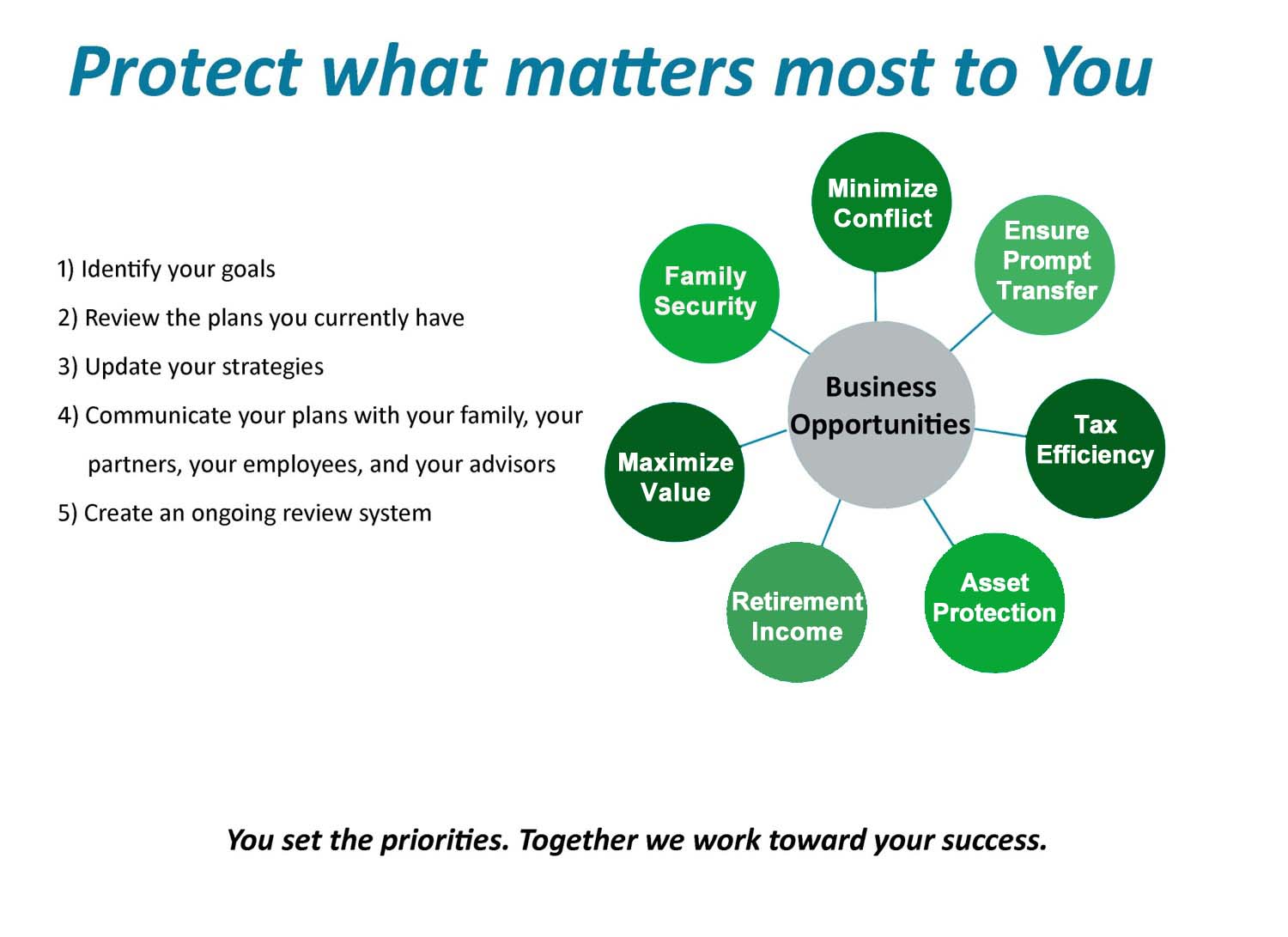

Business Insurance Planning

As a business owner you face many challeges and may have to plan for many contingencies. Life insurance can be a valuable asset for your business. Death Benefit proceeds can inject the capital your business may need in the event of the premature death of an owner or key employee. Policy cash values can help you incentivize your very best employees, as well as create a valuable retirement asset.

- Business Continuation - A capital infusion to aid in the continuation of business in the event of an owner's death or disability

- Succession/Buy Sell Funding - Provides liquidity to purchase the ownership interest of a deceased owner and position the surviving partner with all future control of the business.

- Key Employee - Generates resources to aid in the search for a replacement in the event of a key employee's death.

- Executive Retention - Used in a variety of nonquoalified benefit programs to help attract and retain key employees.

- Debt Protection - Creates a pool of money that can be used to pay off borrowed money.

Supplemental Retirement Plans

The Challenge

Business owners, key employees, and high income earners are finding it more difficult to adequately save for retirement. Why? Qualified retirement plans and group insurance plans, even Social Security, place limits on contributions, payouts and tax advantages of benefits for highly-paid individuals. We may need at least 80 - 100% of pre-retirement income to maintain our current standard of living in retirement.

The Income Gap

With qualified plans and Social Security alone, you and your key employees could receive as little as 30% of your current income at retirement - creating a retirement income gap. Cash values from life insurance can help fill the income gap.

Tax-Efficient Asset Management

Many types of investments produce ordinary or passive income. The taxes on this income are a drag on the net investment return and overall appreciation of the investment. The ability to manage your investment in a tax efficient manner by reducing or eliminating these tax can produce a significantly better tax-equivalent result, along with providing a self-completing tax advantaged death benefit when structured properly.

Integrating Personal and Business Plans

Many business owners have both a personal financial plan and a business financial plan,

|

as well they should. What’s alarming though, is that many people don’t realize the importance of intertwining the two plans. Herein we will explore this relationship in order to better appreciate the business owner's "total economic wealth".

The thoughtfully constructed personal financial plan should include a business plan. In turn, each of the objectives of the business plan affects aspects of the personal financial plan. To look at one plan without considering the other can be detrimental to one’s financial future.

Frequently, after people start a business, they fail to alter their personal financial plans to include ramifications of their business plans. Indeed, even savvy business owners don’t always realize the importance of continually reviewing and updating both plans together.

While accountants often function as the “go to” person for the small business owner, creating financial statements, reviewing costs and implementing tax planning strategies, there are four other areas of financial planning which affect closely held business that I am often called upon by business owners to tackle:

Risk Management: May be viewed as protecting “what you can’t afford to lose”. All potential risks and casualties should be evaluated to determine to what extent the risk should be shifted from the business owner to the insurance company.

To provide adequate protection for the owner, the owner’s family and the business, insurance needs must consider casualty*, life, disability* and health *.

As important as insurance is for the individual, it is even more significant for a closely-held business.

The business owner must consider such types of insurance as key person coverage, to cover the loss of business income upon the death or disability of a key employee; and to fund the buy-out of a deceased shareholder or partner. In addition, casualty* coverage should include business continuation along with fire, theft, and liability*.

Retirement Planning: Makes very clear that personal and business plans are intertwined. For example, a personal plan may be based on the desire to retire at age 65 and sell the business at that time. However, your lifestyle may change and require more earnings upon retirement. This may necessitate changing the business plan to continue the business to provide ongoing income.

For the owner of a closely-held business, succession planning is the key to successful retirement planning. Generally businesses do not fail because of poor tax planning; they often fail, though, because of inadequate or unrealistic succession planning.

If retirement plans are based on income from a business that fails, in all likelihood retirement will be affected drastically. Succession planning is vital to preserve wealth. |

Estate Planning: An important aspect of an estate plan is a succession plan. In most cases the closely-held business represents a large portion of an owner’s estate. If the business is family-held, then the area of gift and estate taxes must be reviewed with particular attention to the owner’s designation of who will “own the business”.

In many instances the owner’s heirs are not qualified or have no interest in running the business, and provisions must be made to protect the business for the estate.

To help develop and implement a realistic plan, a team of professionals should work together: an attorney knowledgeable in estate taxes and business succession plans, an accountant familiar with all aspects of the business, and a financial adviser who understands the fundamentals of business and estate planning, qualified and non-qualified retirement plans. Investment: Affects all financial planning matters. Often the owner of a closely-held business has most of his/her assets tied up in the business. A goal of personal financial planning should be to have assets both in and out of the business. This is especially important if the business or industry is volatile. Investment decisions must factor in the direct correlation between levels of risks and rates of returns. Attributes of an investment that need to be considered include: the amount of risk, rate of return, liquidity, and marketability, as well as also tax considerations. Thus, realizing wealth from a closely-held business can be difficult because of such unplanned – for conditions as changes in government regulations and shifts in the marketplace. The owner of a closely-held business can not separate the business plan from the personal financial plan and vice versa. To be effective and successful, plans must be responsive to changes in goals, economic conditions, legislation and personal circumstances. * Products available through one or more carriers not affiliated with New York Life, dependent on carrier authorization and product availability in your state and locality.

** Please note I do not provide tax, legal, or accounting advice. *** Neither Harris Kagan, nor New York Life Insurance Company, nor its affiliates provides property and casualty insurance. |